Total Plan

January 1, 2024 actuarial valuation results

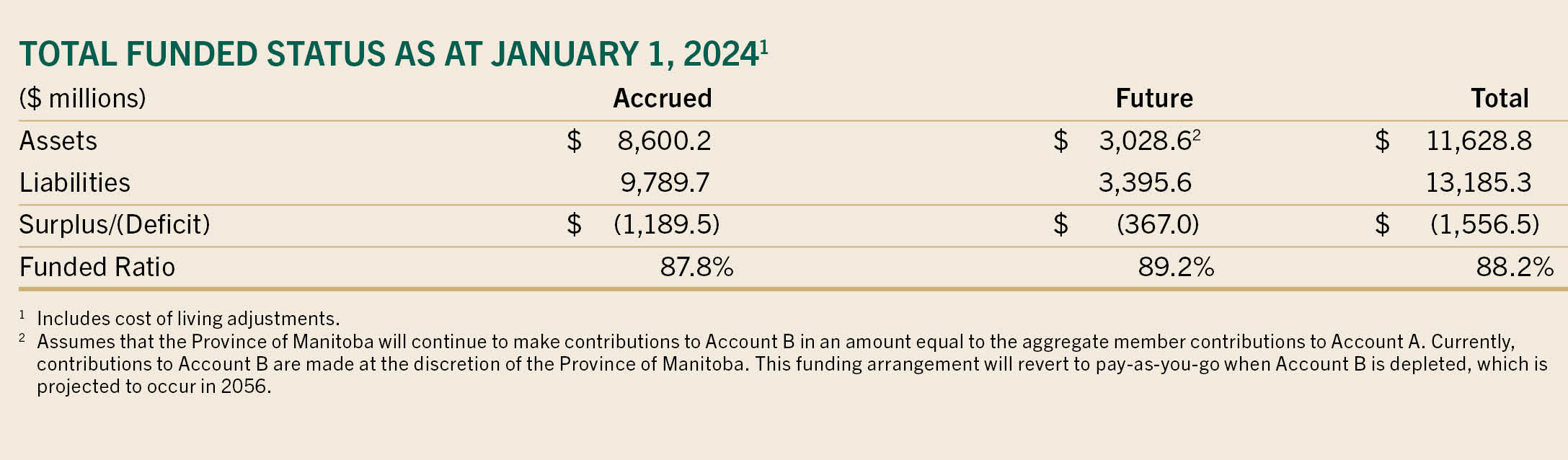

The most recent actuarial valuation of TRAF prepared by the plan actuary was as at January 1, 2024. The valuation results for the total plan (Account A, the Pension Adjustment Account and Account B) are summarized in the following table.

The next actuarial valuation is scheduled to be performed as at January 1, 2027.

January 1, 2025 extrapolated results

The total funded ratio of the plan was extrapolated to be 93.2% as at January 1, 2025. This figure was based on an extrapolation of the January 1, 2024, funded status. An extrapolation incorporates actual investment results, contributions received and benefits paid since the last formal valuation. The limitations are the plan’s actual experience with respect to mortality, retirement and termination since the date of the last valuation (i.e., the extrapolation will continue to rely on assumptions for these variables). The formal actuarial valuation as at January 1, 2024, revealed a total funded ratio of 88.2%. The funded ratio improvement was largely due to the net investment return being greater than the actuarial expected return during 2024.

Actuarial valuation information

Funding valuations, projection valuations, plan actuary funding recommendations, sensitivity analyses and presentations to our stakeholders are available for plan members to view through Online Services.